If you feel like the ground beneath your student loans won’t stop shifting, you aren’t alone. Following months of legal battles, the Biden administration’s Saving on a Valuable Education (SAVE) plan is officially dead. Now, a massive regulatory overhaul is coming to a head, and millions of American borrowers have a crucial choice to make before the government makes it for them.

With the rollout of the Working Families Tax Cuts Act, the federal student loan landscape is undergoing its most significant transformation in a generation. Here is exactly what is changing, what remains of loan forgiveness, and what you need to do to protect your wallet.

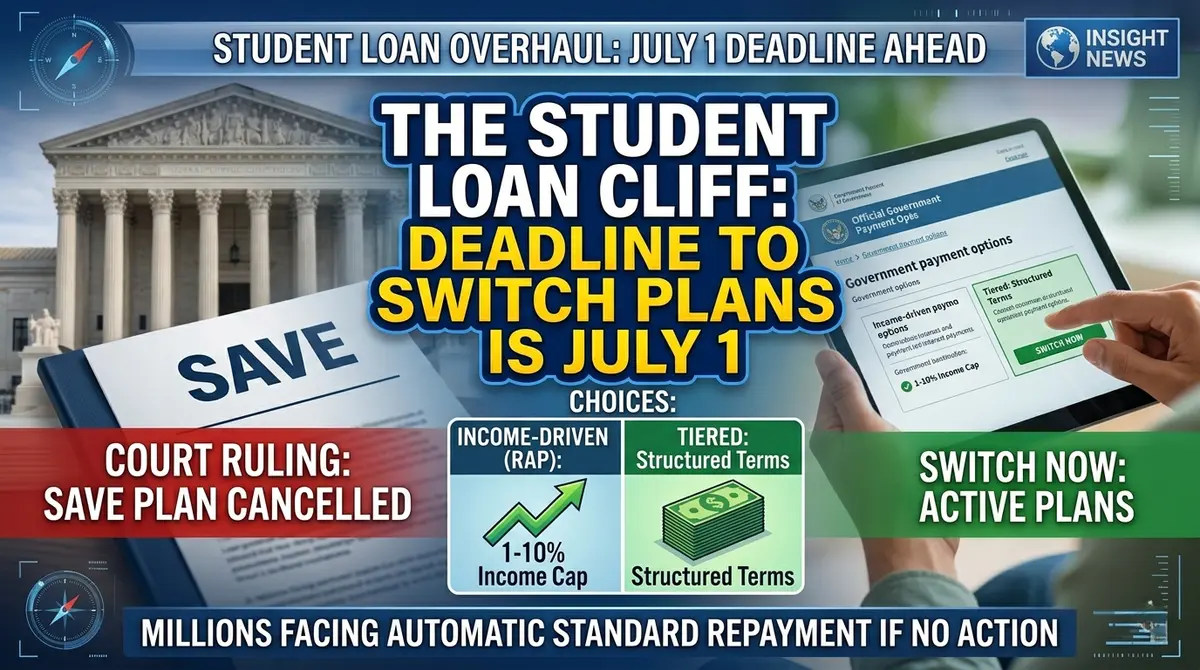

1. The SAVE Plan is Over: Why Your Actions in Next 90 Days Matter

The court ruling on March 10, 2026, permanently vacated the SAVE plan, and the Department of Education is currently contacting the 7.5 million borrowers who were enrolled.

Beginning July 1, loan servicers are issuing official notices giving affected borrowers a 90-day window to manually pick a new, legal repayment option.

The Automatic Penalty: If you do not choose a new plan within your 90-day window, your servicer will automatically place you into a Standard Repayment Plan. For most people, this means your monthly bill could skyrocket.

Furthermore, any payments made while stuck in the recent SAVE forbearance period do not count toward Public Service Loan Forgiveness (PSLF) or Income-Driven Repayment (IDR) forgiveness. To resume making progress toward debt cancellation, you must transition to an active, qualifying plan immediately.

2. Meet the New Plans: RAP and Tiered Standard

Starting July 1, the federal repayment menu is shrinking significantly for new borrowers, while current borrowers are being funneled into a brand-new system. The older options like PAYE and Income-Contingent Repayment (ICR) are being phased out entirely by 2028. Moving forward, the system revolves primarily around two paths:

- The Repayment Assistance Plan (RAP): This is the new primary income-driven option. Monthly payments are capped between 1% and 10% of your adjusted gross income. If you earn less than $10,000 a year, your payment can be as low as $10 a month. A major perk is that on-time payments prevent runaway interest from exploding your balance. However, the horizon for forgiveness under RAP is extended to 30 years.

- The Tiered Standard Repayment Plan: Designed for those who do not qualify for or want an income-driven plan, this structures fixed payments over 10, 15, 20, or 25 years based on your total debt load. It provides lower monthly payments for those with massive balances by spreading the timeline out.

3. What Happens to Student Loan Forgiveness?

While mass cancellation is off the table, targeted forgiveness tracks are still functional but come with critical new catches:

- Public Service Loan Forgiveness (PSLF): This remains fully active, promising complete tax-free debt discharge after 120 qualifying monthly payments for government and non-profit workers. Note that new regulations take effect July 1, tightening rules around employers linked to unlawful activities.

- Income-Based Repayment (IBR): For borrowers with loans disbursed before July 2026, the traditional IBR plan is currently the most legally stable and secure path to 20- or 25-year IDR forgiveness.

- The 2026 Tax Trap: A vital detail to remember is that the American Rescue Plan’s federal tax exemption on forgiven student debt expired on December 31, 2025. Unless an extension is passed, any IDR loan forgiveness processed in 2026 or later will be treated as taxable income by the IRS, potentially leaving you with a hefty bill. (PSLF, disability, and death discharges remain permanently tax-free).

Your Immediate Next Steps

1.Log in to StudentAid.gov

Prerequisite

Check your account dashboard to confirm your current servicer and view the official status of your loans.

2.Use the Loan Simulator Tool

Estimation

Input your current income and family size into the federal simulator to compare what your monthly payment will look like under IBR versus the new RAP format.

3.Submit a New IDR Application

Before your 90-day deadline

Select your new plan manually. Provide electronic consent for the Department of Education to link your IRS tax data directly, which speeds up processing.

4. Maximize the New 1% Auto-Pay Discount

Action by Sept 30, 2026

The standard 0.25% interest rate discount for auto-debit is temporarily bumping up to 1% for eligible borrowers. Ensure you are signed up for auto-pay before September 30 to lock in this deduction through mid-2028.

To better understand the immediate timeline and what this massive overhaul means for your money, you can watch this Important deadline for student loan borrowers video, which breaks down the fast-approaching transition period starting this July.